Twelve Capital has analysed what it could actually mean for a standard 60/40 stocks and bonds investment portfolio when catastrophe bonds are added to the combination, finding even a modest cat bond allocation can improve returns and risk metrics.

Specialist catastrophe bond, insurance-linked securities (ILS) and re/insurance investment manager Twelve Capital had previously checked out the advantages of incorporating insurance subordinated debt into a standard 60/40 portfolio, where 60% is allocated to stocks and 40% to global bonds.

In that case, the investment manager found the inclusion of insurance subordinated debt was helpful and enhanced portfolio efficiency, allowing for greater optimisation of portfolios while enhancing return and Sharpe Ratio, all while maintaining the danger level.

Now, Twelve Capital has undertaken the same evaluation on the results of incorporating catastrophe bonds right into a 60/40 portfolio.

“As a result of their low correlation with traditional financial markets, Cat Bonds provide an efficient tool for optimizing an investor’s risk/return profile,” the investment manager explained.

Adding, “Our research indicates that even modest allocations to Cat Bonds can significantly improve each returns and risk metrics.

“For instance, when publicly available indexes over the past 10 years, a ten% allocation to Cat Bonds has increased the Sharpe Ratio from 0.63 in a standard 60/40 portfolio to 0.74. The same, though more modest, improvement is observed with a 5% allocation to Cat Bonds.”

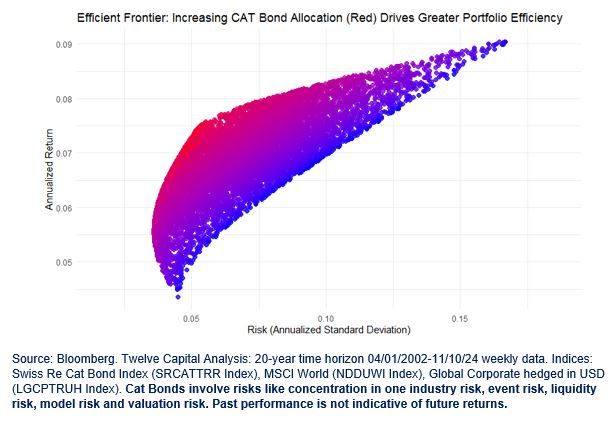

The investment manager continued to elucidate that, “Moreover, for similar level of returns, Cat Bonds can contribute to a discount in overall portfolio risk as highlighted by our evaluation, which uses randomly simulated portfolios, and could be observed within the image below.”

Twelve Capital also said, “Cat Bonds offer several compelling features that make them a beautiful addition to institutional portfolios, including short duration, minimized credit risk, and attractive spreads. These spreads have surged within the wake of recent years’ large-scale catastrophes, now sitting well above those of High Yield Bonds and other alternative asset classes.

“While we acknowledge the differing liquidity levels across asset classes, we’re encouraged by the rapid growth of the Cat Bond market, which is able to support progressively larger allocations in institutional portfolios.”